Contents

General insurers across Australia and New Zealand are operating in one of the most dynamic environments of the past decade.

According to the Heartbeat of General Insurance Report 2025, released by The Bridge International and the Australian and New Zealand Institute of Insurance and Finance (ANZIIF), industry leaders have identified three dominant forces shaping the sector. These findings are based on data from senior insurance professionals (77% in leadership roles) across insurers, brokers, and agencies.

Key Takeaways:

- Economic and regulatory pressure is the number one concern for insurers, driven by claims inflation and rising reinsurance costs

- Australia’s general insurance market is projected to reach $102.8 billion in 2025 - meaning higher premiums for policyholders

- Insurers are using increasingly granular, site-specific data for pricing - two properties on the same street can have very different premiums

- A “set and forget” approach to renewals is risky right now - review your policy terms against the changing market

The Top 3 Industry Concerns:

- Economic and Regulatory Pressures: The leading threat, driven by inflation and compliance.

- Technology Transformation: The urgent need to modernise legacy systems.

- Catastrophe and Climate Exposure: Ongoing risks from extreme weather events.

Why This Matters: For insurance brokers, business owners, and policyholders, these three drivers explain the current landscape of rising pricing, tighter market behavior, and evolving service capabilities.

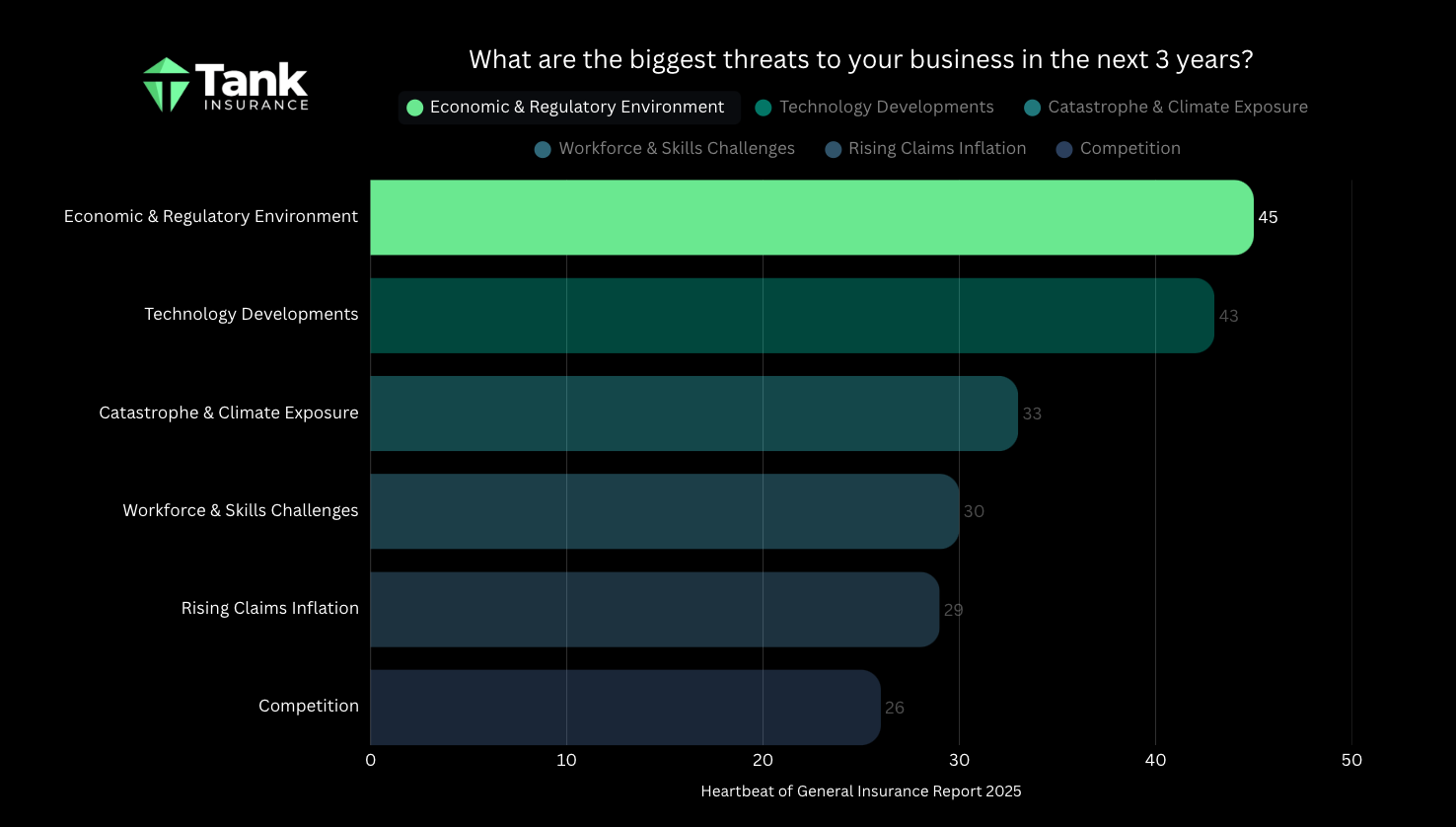

1.What is the Biggest Challenge Facing the General Insurance Industry?

Economic and regulatory pressure is currently ranked as the single largest threat to general insurance, cited by 45% of survey participants.

This pressure is driven by a “perfect storm” of universal factors affecting major insurers:

- Persistent Claims Inflation: Rising costs for parts, raw materials, and skilled labour.

- Reinsurance Costs: Historically high costs from global markets being passed down.

- Regulatory Oversight: Stricter compliance requirements from APRA and ASIC.

As the report notes, these cost pressures and compliance complexities are now outweighing even climate-driven threats in the eyes of insurers.

How Does This Affect Your Insurance Policy?

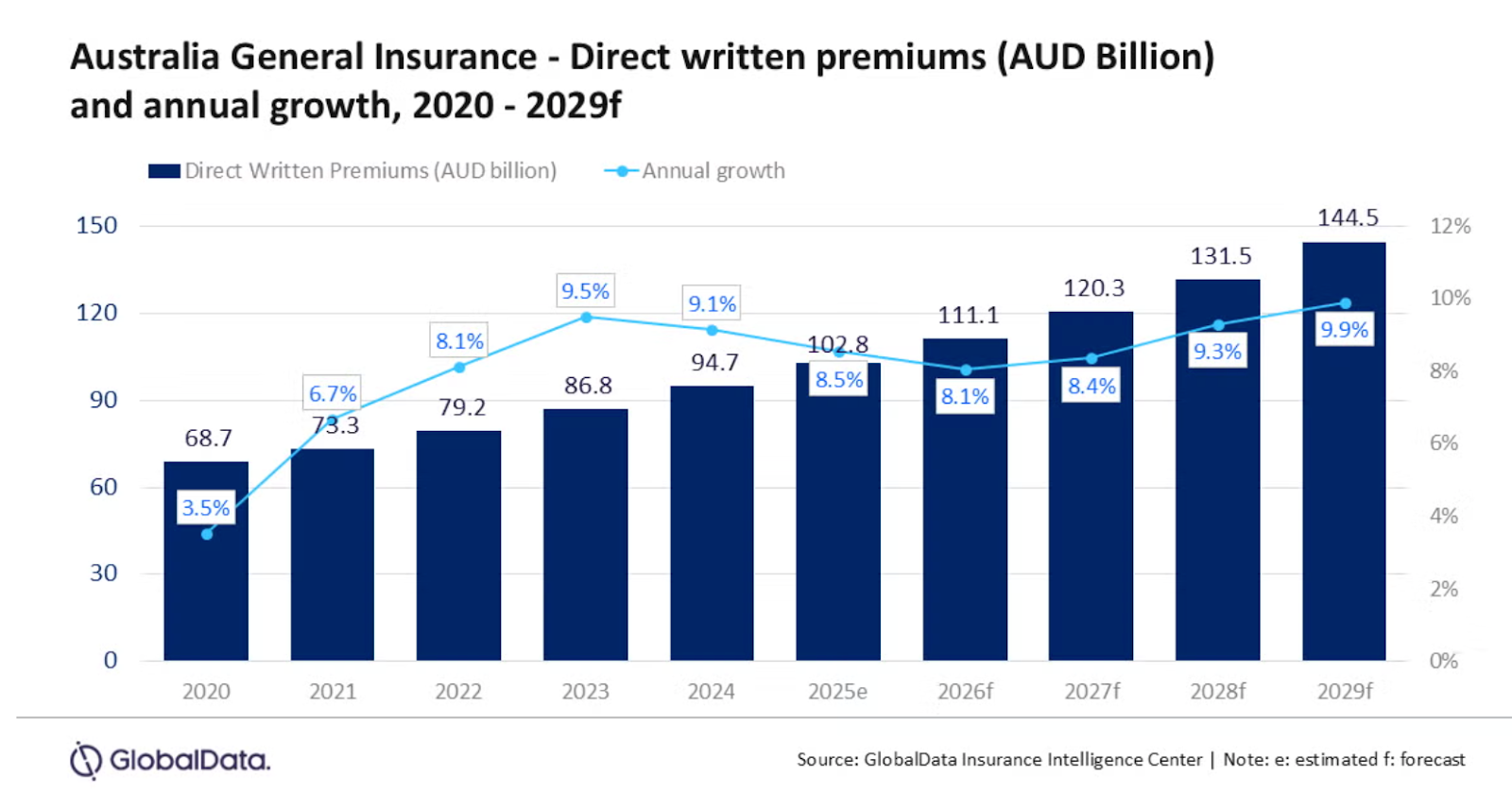

Because insurers must maintain specific capital margins, this economic strain flows directly to the policyholder. In 2025, the Australian general insurance market is projected to reach $102.8 billion, showing an 8.6% increase driven primarily by rising rates.

You can expect:

- Higher Premiums: Costs are being passed on to cover soaring reinsurance and claims inflation.

- Tighter Underwriting: Insurers have a reduced appetite for high-risk zones (like flood plains), leading to stricter conditions.

- Strict Claims Management: While valid claims are paid, insurers are managing repair scopes tighter than ever to control costs.

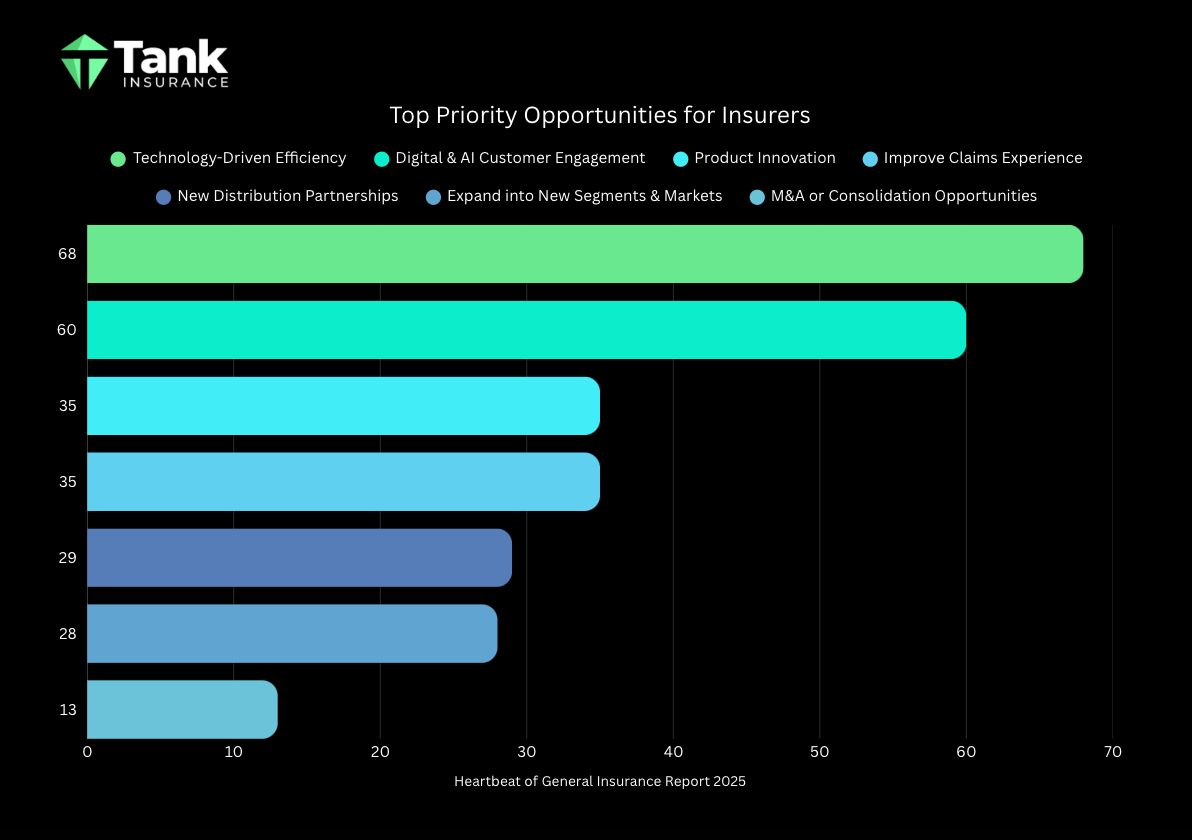

2. How is Technology Transforming the Insurance Industry?

Ranked as the second largest driver of change, technology is viewed by the industry as both a critical solution and a major disruptor.

What are the top technology priorities for insurers?

According to the survey, insurers are focusing their budgets on specific areas to reduce operational expenses and digitise communications:

- Technology-Driven Efficiency (68%): The top priority is streamlining back-end operations.

- AI-Enabled Engagement (60%): Using Artificial Intelligence (AI) to handle customer interactions.

- Data & Analytics: Leveraging data for better product design (35%) and enhanced claims experiences (35%).

The Core Challenge: Many insurers are striving to innovate faster than their legacy IT systems or workforces can adapt, leading to “implementation gaps” across the market.

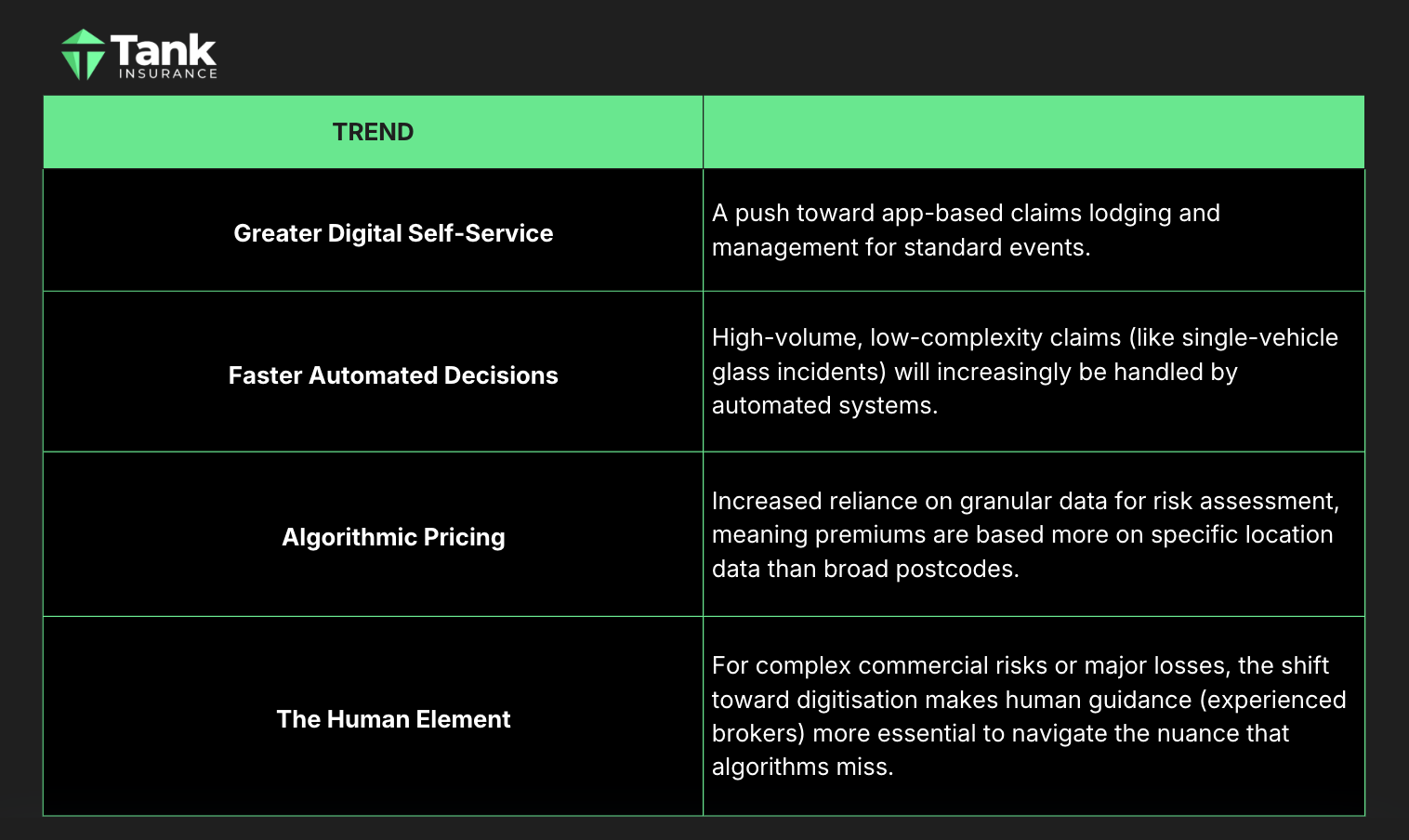

How Will This Tech Shift Affect Policyholders?

Customers will see a continued shift in how they interact with their insurer:

3. How Does Climate Change Affect Insurance Premiums?

The ongoing impact of extreme weather remains a dominant force globally and locally.

Australian insurers are grappling not just with major catastrophe events (like cyclones and bushfires), but increasingly with costly “Secondary Perils.” These include severe convective storms, hail events, and east coast lows, which cumulatively cost the industry billions.

Why does this drive the “Affordability Crisis” in high-risk areas?

This exposure leads to three specific market behaviors:

- Site-Specific Pricing: Insurers are using increasingly granular data. Two properties on the same street may have vastly different premiums based on precise flood modelling or bushfire attack levels.

- Higher Imposed Excesses: To manage exposure, insurers may apply mandatory high excesses specifically for cyclone, flood, or bushfire events in certain regions.

- Reduced Capacity: Some insurers may withdraw from offering new policies entirely in areas deemed to have unmanageable exposure, shrinking the available market for customers in those regions.

Market Outlook: Will Insurance Premiums Rise in 2025?

Despite operational challenges, market financial projections remain robust, driven largely by necessary rate increases.

Projected Premium Growth (2025–2029)

According to 2025 market forecasts by GlobalData, Australia’s general insurance industry is forecast to reach AUD 144.5 billion by 2029, with the market growing at a compound annual growth rate (CAGR) of 8.8% from its 2024 value of AUD 94.7 billion. This growth is measured in terms of direct written premium (DWP).

2025 Premium Forecast:

What This Means for You

The Heartbeat of General Insurance Report 2025 highlights a market defined by economic pressure, rapid tech transformation, and tightening capacity. While every policy is different, these industry-wide trends suggest a challenging environment for policyholders in the coming year.

Key Market Indicators:

- Upward Pressure on Premiums: Industry forecasts indicate that rising reinsurance and claims costs are likely to sustain premium growth across Property, Motor, and Liability lines.

- Tighter Risk Selection: In high-risk zones (particularly for flood or bushfire), insurers are applying stricter underwriting criteria. Securing coverage in these areas may require more detailed risk information than in previous years.

- Data-Driven Adjustments: With the shift toward algorithmic pricing, premiums are becoming increasingly site-specific. This means broad suburb trends matter less than the specific data points of your individual property or business activities.

- The “Digital vs. Human” Balance: While simple claims may move to automated apps, the complexity of the current market makes professional advice critical for ensuring your coverage actually matches your risk.

Is Your Policy Still Competitive?

Given the rapid shifts in insurer risk appetites and pricing models, a “set and forget” approach to renewals is risky in 2025. Your current renewal offer may not reflect the full range of options available in the wider market.

Don’t assume your current policy is the only option. Let Tank Insurance review your current terms against the changing landscape. We help you navigate these industry shifts to find a balance of competitive pricing and robust protection. Contact us or get your quote now.