Contents

Australia’s insurance industry is experiencing a subtle but significant shift. As insurers introduce a non-binary gender option into their quoting systems, they are facing a complex challenge that goes to the core of how premiums are calculated. This change is prompting deeper discussions about data accuracy, social equity, and the future of gender-based pricing.

Because gender remains one of the factors used to determine premiums, these changes matter to every policyholder. Understanding how the industry is adapting helps consumers make informed decisions and navigate a market that is becoming more dynamic and nuanced.

Key Takeaways:

- Some insurers now offer a non-binary gender option, and tests show it can produce a lower premium than the male rate on identical quotes

- The pricing gap exists because insurers have minimal claims data for non-binary policyholders

- Gender is only one rating factor among many - your claims history, age, vehicle type, and location all have a bigger impact

- Always ensure your disclosed information is accurate and consistent with insurer requirements

The Controversy: A Pricing Gap Emerges

The current discussion was triggered when some major insurers offering comprehensive car insurance (including NRMA and Allianz) introduced a non-binary gender option in their online quoting systems.

Following this introduction, public tests have shown that selecting the non-binary option often results in a premium that is lower than the highest binary rate (male) on otherwise identical quotes.

While the exact pricing result is inconsistent across insurers and risk segments, common patterns observed include:

- Male: Generally the highest premium rate (especially for younger drivers).

- Female: Generally the lowest premium rate.

- Non-Binary: The premium is frequently set equal to the lowest binary rate (female), though some quotes show it as marginally lower than both.

This inconsistency raises questions across the industry. Some view the new option as a natural part of modernising customer data. Others question whether the lower pricing has a robust actuarial basis or whether it leads to short-term discrepancies between customers providing the same fundamental risk profile.

Why Prices Differ: The Actuarial Data Gap

Insurance pricing is built on statistical modeling. For decades, insurers have collected binary gender data and linked it to observed claims outcomes.

Established Binary Trends

- Male drivers, particularly younger groups, historically record higher accident rates, leading to higher premiums.

- Women, on average, have different risk profiles in categories like life insurance and annuities. These well-established datasets inform today’s pricing structures.

Non-Binary Data: Minimal or Newly Emerging Because non-binary gender information has only recently begun appearing in insurance applications, insurers have very limited claims data to anchor premium models.

This creates a practical challenge: how to include the non-binary option while avoiding speculative or discriminatory pricing.

Common Interim Solutions

In the absence of established claims history, some insurers have adopted temporary methods such as:

- Defaulting to the lower binary rate (e.g., pricing it the same as the female rate).

- Averaging male and female rates.

- Using proxy risk assumptions until a credible dataset forms.

Insurers generally describe these methods as placeholders, with refinements planned as more reliable data becomes available.

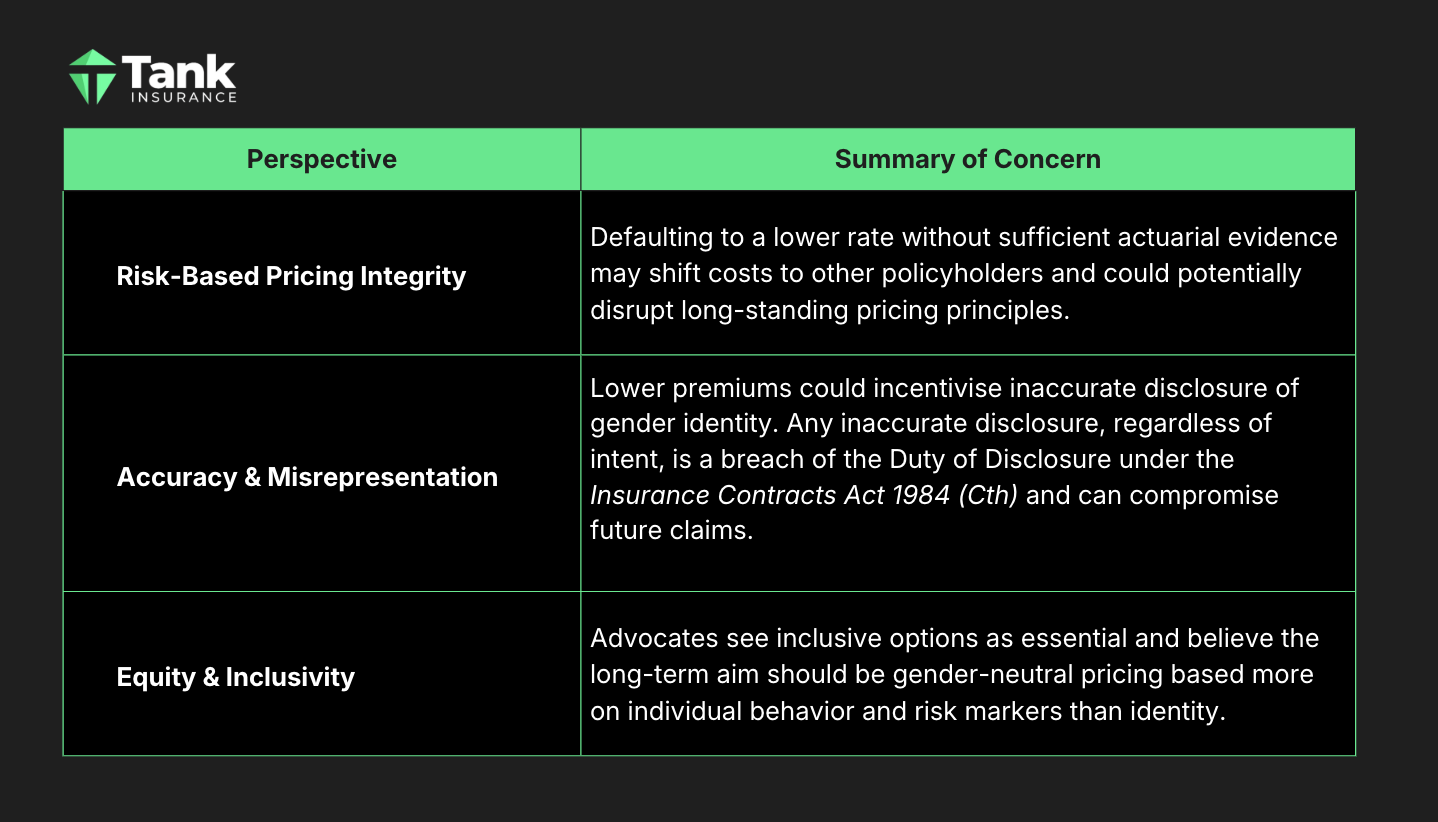

Key Concerns: Fairness, Accuracy, and Long-Term Integrity

This debate has surfaced a range of viewpoints, all centered around accuracy, fairness, and responsible pricing.

While perspectives differ, the common thread is that the current pricing landscape is transitional.

What This Means for Customers

This moment reinforces an ongoing industry trend: insurance pricing is becoming more complex, and online quotes don’t always tell the full story.

- Varying Insurer Policies: Some insurers offer non-binary options; others are still reviewing their systems. Those who do offer the option may price it differently due to their unique interim methodology.

- Accuracy is Paramount: Customers must ensure all disclosed information, including gender identity, is accurate and consistent with insurer requirements, as misrepresentation can legally lead to a reduced claim payout or policy cancellation.

- Focus on True Risk Drivers: Your premium is shaped far more by quantifiable factors like: claims history, age and experience, vehicle and usage, location, and security features. Gender is only one rating factor among many.

Need help with insurance?

Speak with Tank Insurance today. Our team will review your policy, compare the market, and ensure we provide you with competitive terms and pricing.

Get expert advice, and let us help you secure the right cover at the right price.